Bitcoin (BTC) and Ethereum (ETH) experienced significant price surges Sunday night into Monday, reaching their highest levels in over a month.

Key Takeaway #2

However, the rally in proved to be short lived. Trading volumes remained relatively light, and the expectation that ETFs would invigorate the cryptocurrency market with increased interest and capital influx seems to have been overstated as the market pulled back toward unchanged.

Key Takeaway #3

This morning's non-farm payroll report indicated the US economy created 336k jobs in September – almost twice the expected number. Coupled with rising rates, this news initially led to a pullback in most risk assets, including cryptos.

Key Takeaway #4

At the time of writing, however the markets have recovered and are up roughly 1.5% on the day.

Bitcoin (BTC) and Ethereum (ETH) experienced significant price surges Sunday night into Monday, reaching their highest levels in over a month. Many attributed these gains to the launch of several ETH futures ETFs on Monday and the historic seasonality of cryptocurrency price movements in October, humorously referred to as “Uptober.”

Additionally, liquidations in an illiquid futures market again played a role in the rally, with around 30,000 bearish bets liquidated totaling over $100 million. Implied Volatility saw a pop in the front end of about 3%, with the buying of November 1900 calls in ETH and December 32,000 calls in BTC. However, the rally in proved to be short lived. Trading volumes remained relatively light, and the expectation that ETFs would invigorate the cryptocurrency market with increased interest and capital influx seems to have been overstated as the market pulled back toward unchanged.

Despite the favorable cost of gamma exposure and the presence of noteworthy realized volatility, implied volatility has struggled to maintain any upward momentum in the near-term. This market behavior characterizes a particular regime in which observed price movements tend to be short-lived, with limited expectations for sustained continuation. With the market rallying into an area of length for most dealers, especially in the case of ETH, most market makers found themselves already holding long option positions. Consequently, the interest in acquiring additional length at higher vol levels is non-existent and lacking the presence of sustained buying from paper, bids adjust downward to resulting in a reduction in implied volatility.

The ongoing presence of a significant ETH call overwriter has significantly influenced this situation. On Thursday, this participant sold more than 85,000 November 1700 and 1750 call options. This activity not only exerted downward pressure on IV, but also caused a noteworthy shift in the 25D front-end skew. Specifically, the skew shifted from trading at a call premium on Monday to a 19% put premium by Thursday.

This morning's non-farm payroll report indicated the US economy created 336k jobs in September – almost twice the expected number. Coupled with rising rates, this news initially led to a pullback in most risk assets, including cryptos. At the time of writing, however the markets have recovered and are up roughly 1.5% on the day.

Although implied vol has contracted, it's important to note that the breakevens in the front end of the curve are being achieved nearly every day, and occasionally even at rates three to four times the norm. Tuning out the noise around the yield generating call selling and effectively managing gamma exposure, maintaining positions at these levels has proven profitable. Our recommendation is to maintain a long position in the October and November contracts.

Premium Content

Unlock exclusive insights with our cutting-edge digital finance platform. Gain access to next-gen data analytics and digital asset products crafted with applied science. Subscribe now to stay ahead of the curve.

Bitcoin (BTC) and Ethereum (ETH) experienced significant price surges Sunday night into Monday, reaching their highest levels in over a month. Many attributed these gains to the launch of several ETH futures ETFs on Monday and the historic seasonality of cryptocurrency price movements in October, humorously referred to as “Uptober.”

Additionally, liquidations in an illiquid futures market again played a role in the rally, with around 30,000 bearish bets liquidated totaling over $100 million. Implied Volatility saw a pop in the front end of about 3%, with the buying of November 1900 calls in ETH and December 32,000 calls in BTC. However, the rally in proved to be short lived. Trading volumes remained relatively light, and the expectation that ETFs would invigorate the cryptocurrency market with increased interest and capital influx seems to have been overstated as the market pulled back toward unchanged.

Despite the favorable cost of gamma exposure and the presence of noteworthy realized volatility, implied volatility has struggled to maintain any upward momentum in the near-term. This market behavior characterizes a particular regime in which observed price movements tend to be short-lived, with limited expectations for sustained continuation. With the market rallying into an area of length for most dealers, especially in the case of ETH, most market makers found themselves already holding long option positions. Consequently, the interest in acquiring additional length at higher vol levels is non-existent and lacking the presence of sustained buying from paper, bids adjust downward to resulting in a reduction in implied volatility.

The ongoing presence of a significant ETH call overwriter has significantly influenced this situation. On Thursday, this participant sold more than 85,000 November 1700 and 1750 call options. This activity not only exerted downward pressure on IV, but also caused a noteworthy shift in the 25D front-end skew. Specifically, the skew shifted from trading at a call premium on Monday to a 19% put premium by Thursday.

This morning's non-farm payroll report indicated the US economy created 336k jobs in September – almost twice the expected number. Coupled with rising rates, this news initially led to a pullback in most risk assets, including cryptos. At the time of writing, however the markets have recovered and are up roughly 1.5% on the day.

Although implied vol has contracted, it's important to note that the breakevens in the front end of the curve are being achieved nearly every day, and occasionally even at rates three to four times the norm. Tuning out the noise around the yield generating call selling and effectively managing gamma exposure, maintaining positions at these levels has proven profitable. Our recommendation is to maintain a long position in the October and November contracts.

1 Year 90 Day Implied Volatility BTC vs ETH

• 90 day Implied Volatility historically traded at a premium to ETH.

• This dynamic changed during the 2nd quarter of 2023 following the Shanghai upgrade.

• The increased liquidity has dampened the long-term volatility and led to more call overwriting in the ETH options markets, driving down Implied Vol.

ATM IV Term Structure

• Contango in both majors remains, with little change in term structure in BTC, while front end ETH came in relative to the backs.

• Approval for multiple ETH futures ETFs had initially led to a narrowing of the vol spread in the front end last week, but reverted after the rally failed Monday.

• BTC continues to trade at a vol premium to ETH, attributable to the anticipation of price appreciation as we approach the halving next April, combined with the consistent overwriting of ETH calls.

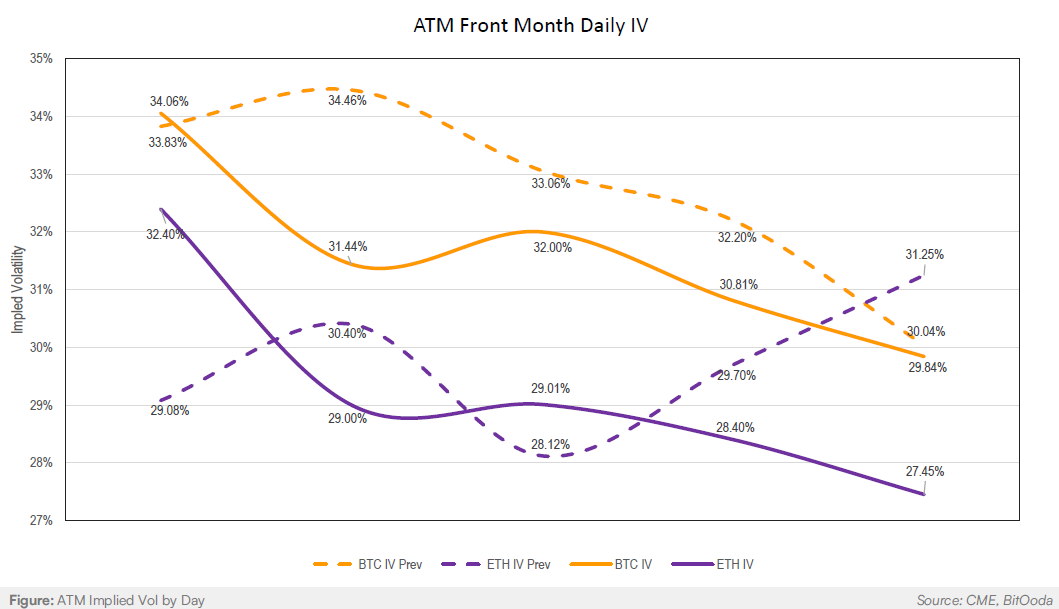

At-the-Money Front Month Daily Implied Volatility

• Front month IV trended lower on the week.

• ETH IV failed to hold a bid after the ETF induced rally never gained steam and settled back toward unchanged.

• 30-day Implied Volatility still remains historically cheap and will likely continue to face pressure, barring a breakout of the recent range-bound trading.

BTC & ETH 25 Delta Skew (30 day)

• Skew continues to be much more volatile than outright implied volatility.

• ETH skew sold off from a slight call premium to a high of 19.4% put premium on Thursday.

• This is a strong indication that much of the paper flow in cryptos is currently speculative paper bidding calls on rallies and puts on selloffs.

Front Month IV Curves

• 1 Month BTC 25 delta puts priced 2.75 vols over ATM, with 25 delta calls priced 1.5 vols over ATM.

• 1 Month ETH 25 delta puts priced 4 vols over ATM, with 25 delta calls priced .75 over ATM.

• BTC exhibits little favor between puts and calls in the front month, while ETH currently represents a significant premium for puts over calls.

ETH 1x2 Call Spread Expiring March 2024

• We will continue to monitor our past two recommended trade strategies in the ETH March ‘24 contract.

• We suggested selling the $2100/$2500 1 by 2 call spread (selling the $2100 call, buying 2 $2500 calls) at flat premium.

• ATM implied volatility in March ’24 stands at 42 % resulting in a current premium of $10 to the two options on the strategy, despite a significant selloff in the futures market.

• We recommend holding the trade at current levels.

ETH 1x2 Iron Butterfly Expiring March 2024

• Monitoring our second recommended strategy of selling one March $1900 Straddle and buying two $1600/$2200 Strangles:

• Similar to the call spread ratio, there was zero outlay of premium.

• Currently this iron butterfly ratio value remains flat.

• We view this as a long-term strategy and recommend holding through year end and adding opportunistically.

This research is only for the clients of BitOoda. This research is not intended to constitute an offer, solicitation, or invitation for any securities and may not be distributed into jurisdictions where it is unlawful to do so. For additional disclosures and information, please contact a BitOoda representative at info@bitooda.io.

Analyst Certification

Michael Tauckus, the research analyst denoted by an “AC” on the cover of this report, hereby certifies that all of the views expressed in this report accurately reflect his personal views, which have not been influenced by considerations of the firm’s business or client relationships.

Conflicts of Interest

This research contains the views, opinions, and recommendations of BitOoda. This report is intended for research and educational purposes only. We are not compensated in any way based upon any specific view or recommendation.

General Disclosures

Any information (“Information”) provided by BitOoda Holdings, Inc., BitOoda Digital, LLC, BitOoda Technologies, LLC or Ooda Commodities, LLC and its affiliated or related companies (collectively, “BitOoda”), either in this publication or document, in any other communication, or on or throughhttp://www.bitooda.io/, including any information regarding proposed transactions or trading strategies, is for informational purposes only and is provided without charge. BitOoda is not and does not act as a fiduciary or adviser, or in any similar capacity, in providing the Information, and the Information may not be relied upon as investment, financial, legal, tax, regulatory, or any other type of advice. The Information is being distributed as part of BitOoda’s sales and marketing efforts as an introducing broker and is incidental to its business as such.BitOoda seeks to earn execution fees when its clients execute transactions using its brokerage services. BitOoda makes no representations or warranties (express or implied) regarding, nor shall it have any responsibility or liability for the accuracy, adequacy, timeliness or completeness of, the Information, and no representation is made or is to be implied that the Information will remain unchanged. BitOoda undertakes no duty to amend, correct, update, or otherwise supplement the Information.

The Information has not been prepared or tailored to address, and may not be suitable or appropriate for the particular financial needs, circumstances or requirements of any person, and it should not be the basis for making any investment or transaction decision. The Information is not a recommendation to engage in any transaction. The digital asset industry is subject to a range of inherent risks, including but not limited to: price volatility, limited liquidity, limited and incomplete information regarding certain instruments, products, or digital assets, and a still emerging and evolving regulatory environment. The past performance of any instruments, products or digital assets addressed in the Information is not a guide to future performance, nor is it a reliable indicator of future results or performance.

All derivatives brokerage is conducted byOoda Commodities, LLC a member of NFA and subject to NFA’s regulatory oversight and examinations. However, you should be aware that NFA does not have regulatory oversight authority over underlying or spot virtual currency products or transactions or virtual currency exchanges, custodians or markets.

BitOoda Technologies, LLC is a member of FINRA.

“BitOoda”, “BitOoda Difficulty”, “BitOoda Hash”, “BitOoda Compute”, and the BitOoda logo are trademarks of BitOoda Holdings, Inc.

Copyright 2023 BitOoda Holdings, Inc. All rights reserved. No part of this material may be reprinted, redistributed, or sold without prior written consent of BitOoda.

Bitcoin (BTC) and Ethereum (ETH) experienced significant price surges Sunday night into Monday, reaching their highest levels in over a month. Many attributed these gains to the launch of several ETH futures ETFs on Monday and the historic seasonality of cryptocurrency price movements in October, humorously referred to as “Uptober.”

Additionally, liquidations in an illiquid futures market again played a role in the rally, with around 30,000 bearish bets liquidated totaling over $100 million. Implied Volatility saw a pop in the front end of about 3%, with the buying of November 1900 calls in ETH and December 32,000 calls in BTC. However, the rally in proved to be short lived. Trading volumes remained relatively light, and the expectation that ETFs would invigorate the cryptocurrency market with increased interest and capital influx seems to have been overstated as the market pulled back toward unchanged.

Despite the favorable cost of gamma exposure and the presence of noteworthy realized volatility, implied volatility has struggled to maintain any upward momentum in the near-term. This market behavior characterizes a particular regime in which observed price movements tend to be short-lived, with limited expectations for sustained continuation. With the market rallying into an area of length for most dealers, especially in the case of ETH, most market makers found themselves already holding long option positions. Consequently, the interest in acquiring additional length at higher vol levels is non-existent and lacking the presence of sustained buying from paper, bids adjust downward to resulting in a reduction in implied volatility.

The ongoing presence of a significant ETH call overwriter has significantly influenced this situation. On Thursday, this participant sold more than 85,000 November 1700 and 1750 call options. This activity not only exerted downward pressure on IV, but also caused a noteworthy shift in the 25D front-end skew. Specifically, the skew shifted from trading at a call premium on Monday to a 19% put premium by Thursday.

This morning's non-farm payroll report indicated the US economy created 336k jobs in September – almost twice the expected number. Coupled with rising rates, this news initially led to a pullback in most risk assets, including cryptos. At the time of writing, however the markets have recovered and are up roughly 1.5% on the day.

Although implied vol has contracted, it's important to note that the breakevens in the front end of the curve are being achieved nearly every day, and occasionally even at rates three to four times the norm. Tuning out the noise around the yield generating call selling and effectively managing gamma exposure, maintaining positions at these levels has proven profitable. Our recommendation is to maintain a long position in the October and November contracts.

1 Year 90 Day Implied Volatility BTC vs ETH

• 90 day Implied Volatility historically traded at a premium to ETH.

• This dynamic changed during the 2nd quarter of 2023 following the Shanghai upgrade.

• The increased liquidity has dampened the long-term volatility and led to more call overwriting in the ETH options markets, driving down Implied Vol.

ATM IV Term Structure

• Contango in both majors remains, with little change in term structure in BTC, while front end ETH came in relative to the backs.

• Approval for multiple ETH futures ETFs had initially led to a narrowing of the vol spread in the front end last week, but reverted after the rally failed Monday.

• BTC continues to trade at a vol premium to ETH, attributable to the anticipation of price appreciation as we approach the halving next April, combined with the consistent overwriting of ETH calls.

At-the-Money Front Month Daily Implied Volatility

• Front month IV trended lower on the week.

• ETH IV failed to hold a bid after the ETF induced rally never gained steam and settled back toward unchanged.

• 30-day Implied Volatility still remains historically cheap and will likely continue to face pressure, barring a breakout of the recent range-bound trading.

BTC & ETH 25 Delta Skew (30 day)

• Skew continues to be much more volatile than outright implied volatility.

• ETH skew sold off from a slight call premium to a high of 19.4% put premium on Thursday.

• This is a strong indication that much of the paper flow in cryptos is currently speculative paper bidding calls on rallies and puts on selloffs.

Front Month IV Curves

• 1 Month BTC 25 delta puts priced 2.75 vols over ATM, with 25 delta calls priced 1.5 vols over ATM.

• 1 Month ETH 25 delta puts priced 4 vols over ATM, with 25 delta calls priced .75 over ATM.

• BTC exhibits little favor between puts and calls in the front month, while ETH currently represents a significant premium for puts over calls.

ETH 1x2 Call Spread Expiring March 2024

• We will continue to monitor our past two recommended trade strategies in the ETH March ‘24 contract.

• We suggested selling the $2100/$2500 1 by 2 call spread (selling the $2100 call, buying 2 $2500 calls) at flat premium.

• ATM implied volatility in March ’24 stands at 42 % resulting in a current premium of $10 to the two options on the strategy, despite a significant selloff in the futures market.

• We recommend holding the trade at current levels.

ETH 1x2 Iron Butterfly Expiring March 2024

• Monitoring our second recommended strategy of selling one March $1900 Straddle and buying two $1600/$2200 Strangles:

• Similar to the call spread ratio, there was zero outlay of premium.

• Currently this iron butterfly ratio value remains flat.

• We view this as a long-term strategy and recommend holding through year end and adding opportunistically.

This research is only for the clients of BitOoda. This research is not intended to constitute an offer, solicitation, or invitation for any securities and may not be distributed into jurisdictions where it is unlawful to do so. For additional disclosures and information, please contact a BitOoda representative at info@bitooda.io.

Analyst Certification

Michael Tauckus, the research analyst denoted by an “AC” on the cover of this report, hereby certifies that all of the views expressed in this report accurately reflect his personal views, which have not been influenced by considerations of the firm’s business or client relationships.

Conflicts of Interest

This research contains the views, opinions, and recommendations of BitOoda. This report is intended for research and educational purposes only. We are not compensated in any way based upon any specific view or recommendation.

General Disclosures

Any information (“Information”) provided by BitOoda Holdings, Inc., BitOoda Digital, LLC, BitOoda Technologies, LLC or Ooda Commodities, LLC and its affiliated or related companies (collectively, “BitOoda”), either in this publication or document, in any other communication, or on or throughhttp://www.bitooda.io/, including any information regarding proposed transactions or trading strategies, is for informational purposes only and is provided without charge. BitOoda is not and does not act as a fiduciary or adviser, or in any similar capacity, in providing the Information, and the Information may not be relied upon as investment, financial, legal, tax, regulatory, or any other type of advice. The Information is being distributed as part of BitOoda’s sales and marketing efforts as an introducing broker and is incidental to its business as such.BitOoda seeks to earn execution fees when its clients execute transactions using its brokerage services. BitOoda makes no representations or warranties (express or implied) regarding, nor shall it have any responsibility or liability for the accuracy, adequacy, timeliness or completeness of, the Information, and no representation is made or is to be implied that the Information will remain unchanged. BitOoda undertakes no duty to amend, correct, update, or otherwise supplement the Information.

The Information has not been prepared or tailored to address, and may not be suitable or appropriate for the particular financial needs, circumstances or requirements of any person, and it should not be the basis for making any investment or transaction decision. The Information is not a recommendation to engage in any transaction. The digital asset industry is subject to a range of inherent risks, including but not limited to: price volatility, limited liquidity, limited and incomplete information regarding certain instruments, products, or digital assets, and a still emerging and evolving regulatory environment. The past performance of any instruments, products or digital assets addressed in the Information is not a guide to future performance, nor is it a reliable indicator of future results or performance.

All derivatives brokerage is conducted byOoda Commodities, LLC a member of NFA and subject to NFA’s regulatory oversight and examinations. However, you should be aware that NFA does not have regulatory oversight authority over underlying or spot virtual currency products or transactions or virtual currency exchanges, custodians or markets.

BitOoda Technologies, LLC is a member of FINRA.

“BitOoda”, “BitOoda Difficulty”, “BitOoda Hash”, “BitOoda Compute”, and the BitOoda logo are trademarks of BitOoda Holdings, Inc.

Copyright 2023 BitOoda Holdings, Inc. All rights reserved. No part of this material may be reprinted, redistributed, or sold without prior written consent of BitOoda.